Heat and low rainfall shift NSW market dynamics

Key points

- NSW has faced dry, hot conditions, prompting earlier decisions from producers.

- More cows and cow-and-calf units hit NSW saleyards.

- Higher cow supply and selective buyers put downward pressure on prices.

Over the past two years, seasonal conditions have increasingly diverged across Australia. While northern regions have generally benefited from better rainfall, the south has faced tighter feed conditions. NSW, in recent months, has seen a shift in season and a clear change in supply dynamics into markets, particularly in breeding females.

NSW season turns and producers respond

NSW held up relatively well through much of 2025. However, since October 2025, rainfall has been patchy and, in many areas, below seasonal averages. The Bureau of Meteorology (BOM) reported NSW’s area-averaged January rainfall at 27.2mm (59% below the 1961–1990 average), making it the driest January since 2014. Heat also intensified, with NSW recording its second-warmest January average maximum temperature on record. Due to slowing pasture growth and tightening feed availability, producers are making earlier management decisions to stay ahead of conditions.

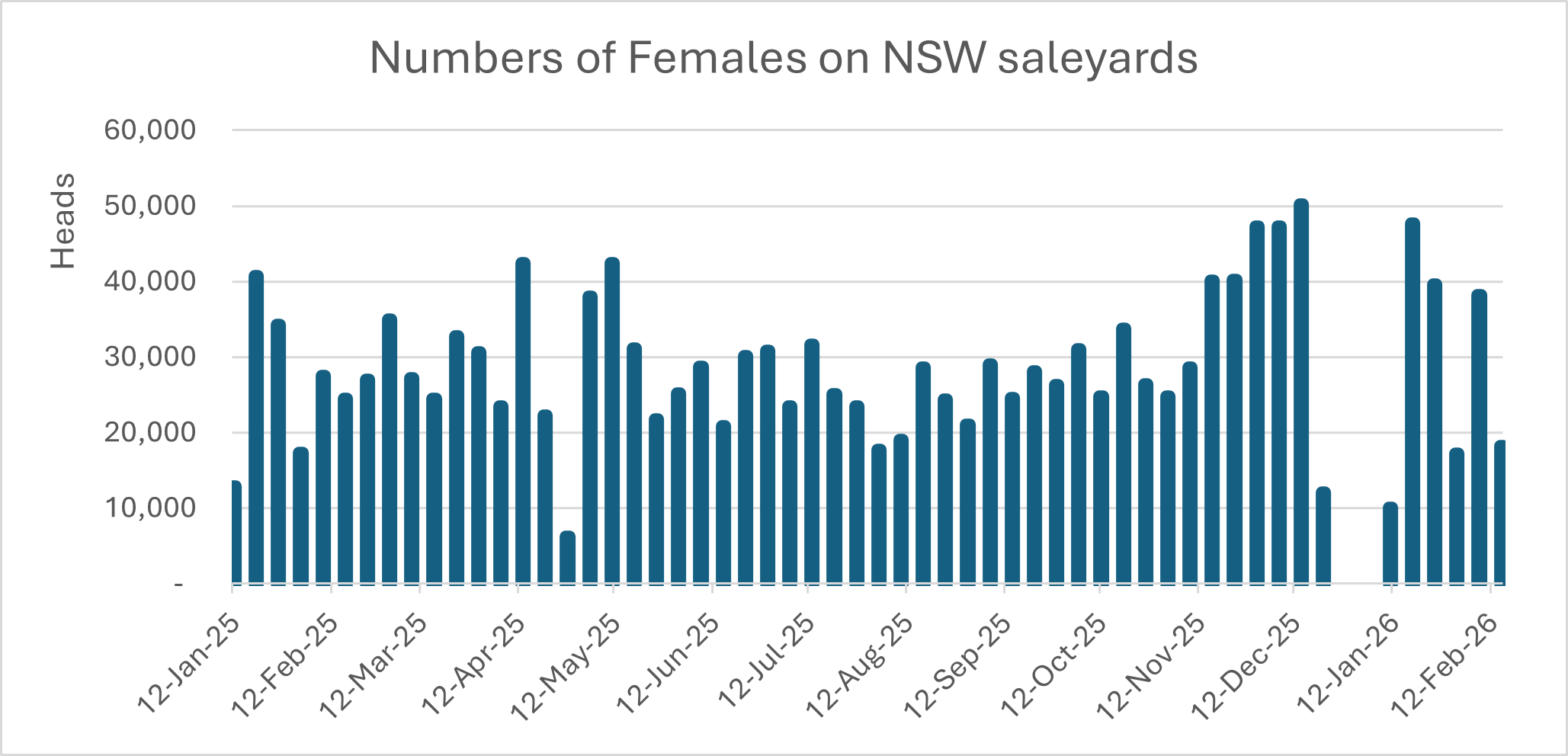

That response is now showing up in saleyard flows. In recent weeks, NSW saleyards have recorded higher numbers of cows – as well as more cow-and-calf units – than is typical for this time of year. Markets such as Dubbo and Wagga have yarded larger lines of cows accompanied by weaner calves, signalling an increase in female offloading as producers reduce stocking pressure ahead of further pasture decline.

Source: NLRS

Rising cow supply reshapes saleyard mix

The increase in cows coming to market has changed the tone of the sale. While demand remains present, a larger share of processing-type cattle in the mix has increased competition on the supply side, particularly where quality and condition vary.

Cow-and-calf units tend to attract a narrower buyer pool, which contributes to price sensitivity when numbers lift quickly. As a result, price outcomes have become more dependent on presentation and buyer attendance than earlier in the year, when supply was tighter.

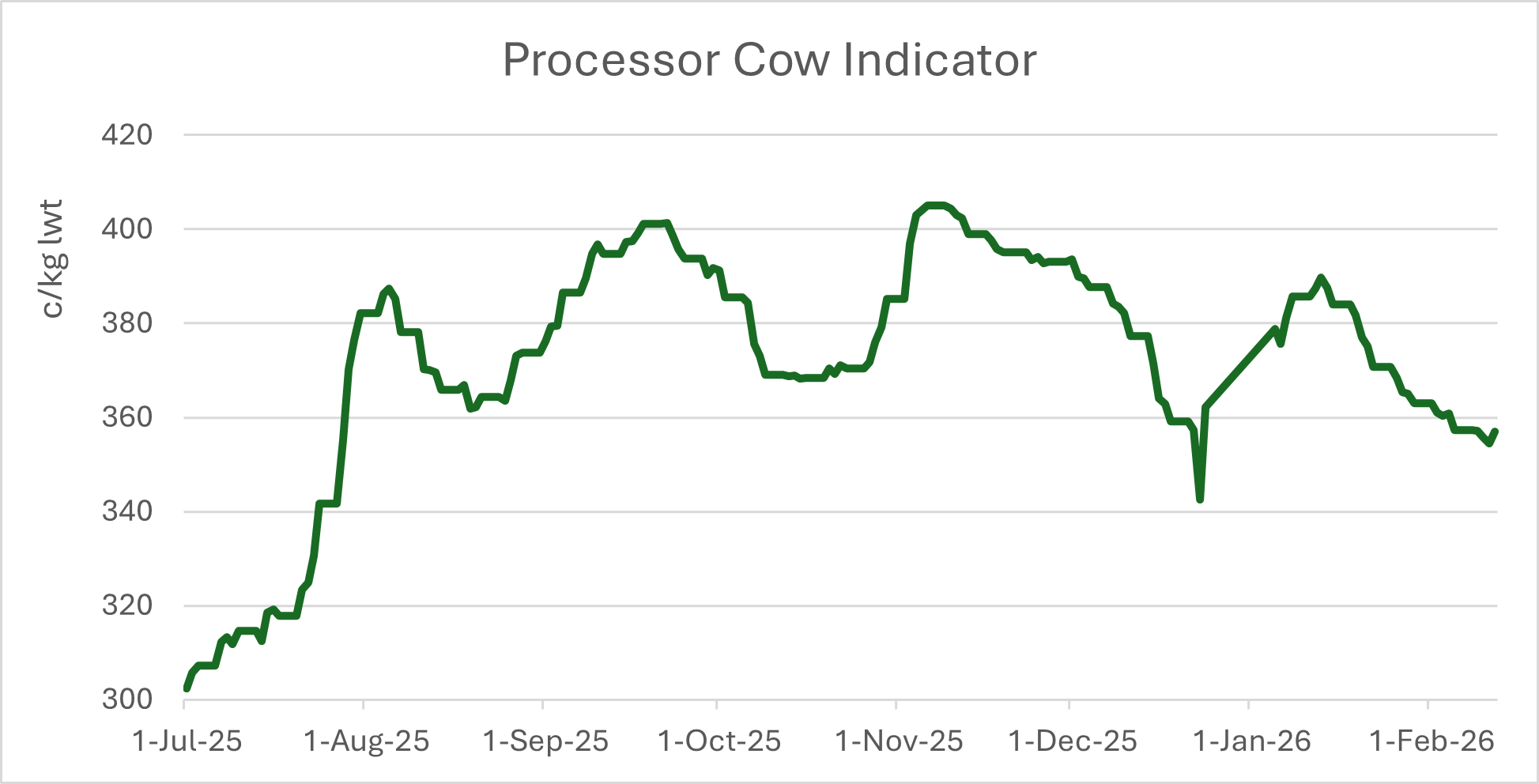

Source: NLRS

The higher flow of female cattle has weighed on processor cow prices. In NSW, the Processor Cow Indicator peaked at 405¢/kg liveweight (lwt) in November, before easing to 356¢/kg lwt by the second week of February. This softening trend in price aligns with the increased availability of cows through saleyards.

Market volatility has also been a feature of recent weeks. Following the New Year period, saleyards returned with the usual post-break lift in yardings. However, the Australia Day public holiday, combined with extreme heat, led to cancellations and disrupted the rhythm of supply. That uneven flow has contributed to greater variability in both yardings and prices from week to week, with the industry appropriately prioritising animal welfare during the heat events.

To watch during the next week

If patchy rainfall persists and pasture conditions continue to tighten, female supply is likely to remain elevated in the near term. However, if the widespread rain forecasted for the coming days materialises, it may quickly shape the female supply to the opposite.

Attribute to: Emiliano Diaz, Senior Market Information Analyst

Information is correct at time of publication on 13 February 2026.