Smaller flock sharpens shift in production focuses

Key points

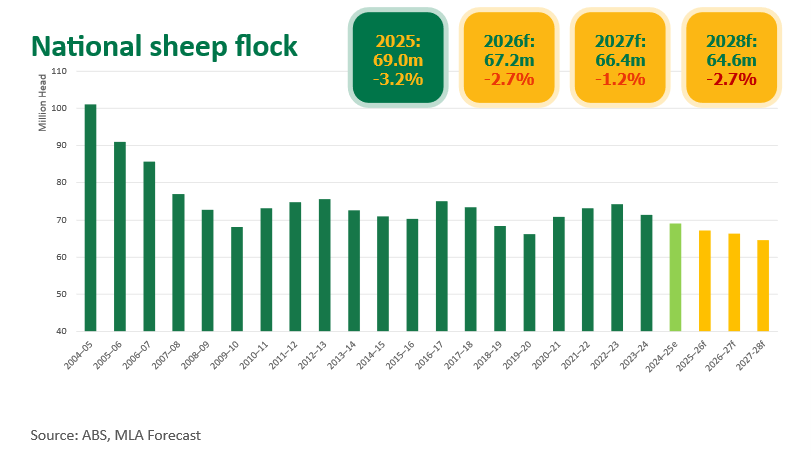

- The national sheep flock is forecast to fall to 67.1 million head in 2026.

- Lower lamb and sheep slaughter will tighten supply.

- Feed management, breeder retention and enterprise flexibility are shaping up to be critical for 2026.

Australia’s sheep industry is heading into 2026 with tighter supply and reduced flock-level flexibility, particularly across southern production regions. The national flock is forecast to decline 2.7% to 67.1 million head, reflecting ongoing seasonal pressure and several years of elevated turn-off.

For producers, the key takeaway is that rebuild options are likely to remain limited in the short-term.

Dry conditions across Victoria, SA, Tasmania and southern NSW continue to weigh on pasture availability, fodder reserves and confidence. While recent rainfall has offered some relief in parts, many producers remain cautious around stocking rates, retention and replacement decisions.

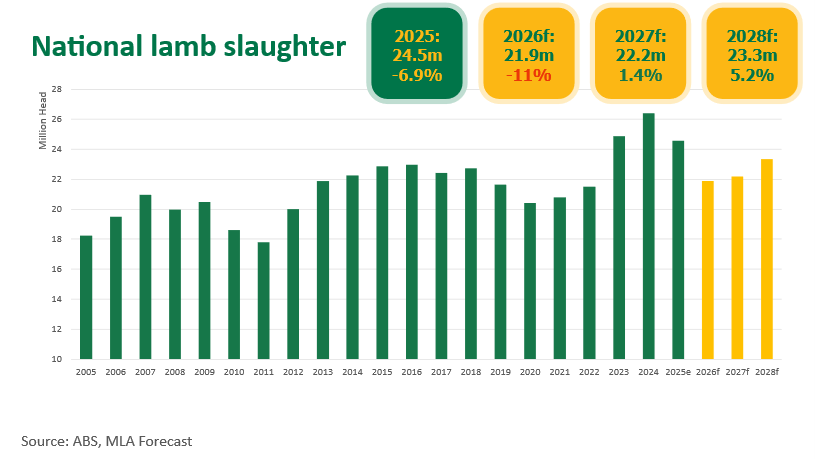

This caution is reflected in the 2026 slaughter outlook. Lamb slaughter is forecast to fall 11% to 21.86 million head, while sheep slaughter is forecast to decline 30% to 7.13 million head. This points to a smaller pool of available stock and a slower pathway to rebuilding. Heavy turn-off in recent years – including breeding females – has reduced the industry’s immediate ability to lift numbers.

On farm, this means flock decisions will hinge on seasonal confidence. Producers with tight feed supply may weigh up whether to retain breeders, sell earlier, or adjust their enterprise mix to manage risk and cash flow. In many regions, meaningful flock rebuilding is unlikely until feed conditions improve more broadly and consistently.

Production is expected to remain relatively resilient despite reduced slaughter, supported by continued gains in average carcase weights. Lamb production is forecast to ease 10% to 537,000 tonnes carcase weight (cwt), while mutton production is expected to fall 29% to 184,770 tonnes cwt. This underscores the value of finishing systems that maintain performance when numbers tighten. Ongoing improvements in genetics, grain feeding, containment feeding and demand for heavier lambs will continue to support this trend.

Wool is also re-emerging as an important part of the production equation. Stronger wool prices are improving returns from Merino enterprises, potentially encouraging producers to retain sheep where conditions allow. For Merino and mixed-enterprise operations, this shift could increasingly influence flock structure and retention decisions over the next 12 months.

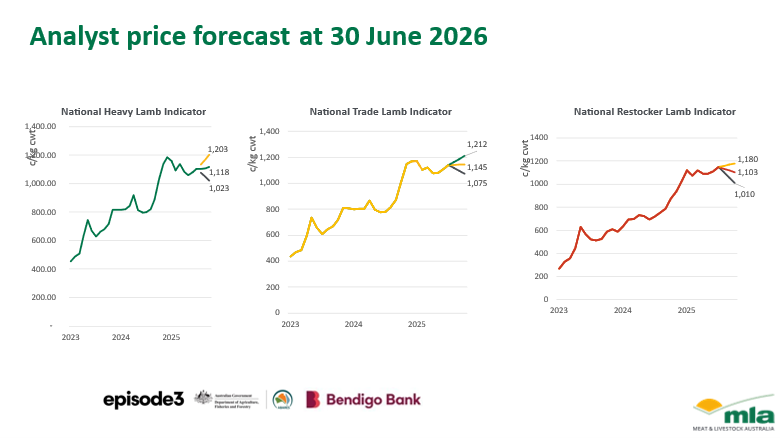

Finished lamb prices are expected to remain firm, though restocker demand may stay softer if seasonal conditions remain uneven. The outlook suggests 2026 will be a year where management matters as much as market direction. Feed budgeting, protecting core breeders and targeting weight and market specifications are likely to be more important than chasing volume.

Overall, 2026 is shaping up as a year to protect flexibility. Tighter sheep numbers and mixed seasonal conditions are likely to keep rebuild decisions cautious, while strong finished markets continue to reward weight, timing and meeting specification. Businesses that manage feed carefully, retain productive breeders and maintain finishing performance are likely to be better placed to respond when seasonal confidence lifts.

Find out more about 2026 Sheep Industry Projections and watch the webinar.

Attribute content to: Emiliano Diaz, MLA Senior Market Information Analyst

Information is correct at time of publication on 2 April 2026.