Restocker premium narrows as seasonal pressure lifts cattle supply

Key points

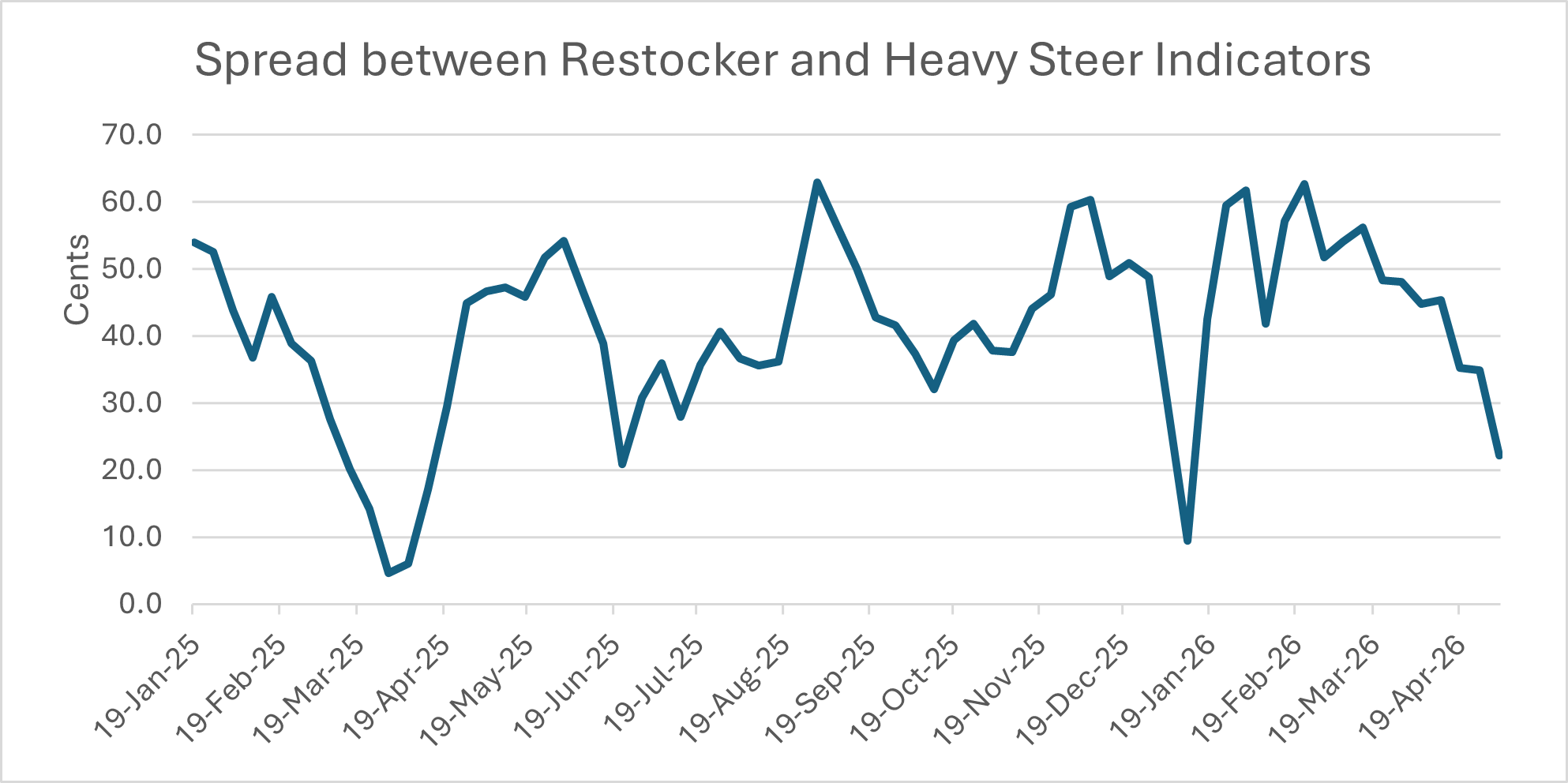

- The spread between heavy steers and restocker yearling steers has narrowed to the lowest since June 2025.

- Restocker demand has softened as weather conditions deteriorate in NSW.

- Finished cattle remain supported by processor activity and strong global demand for Australian beef.

The spread between heavy steers and restocker yearling steers has narrowed materially since February, highlighting how the market is valuing cattle through autumn.

This week, the National Heavy Steer Indicator sat at 417.6¢/kg liveweight (lwt), while the National Restocker Yearling Steer Indicator was at 439.8¢/kg lwt. This leaves a spread of 22.2¢/kg lwt in favour of restocker yearling steers – the lowest since June 2025.

In February, the Heavy Steer Indicator was 440.6¢/kg lwt and the Restocker Yearling Steer Indicator was 503.3¢/kg lwt, leaving a much wider spread of 62.7¢/kg lwt.

While the spread remains positive for restockers, it has tightened significantly from earlier in the year and sits below the 2025 average of around 40¢/kg lwt. In practical terms, the market is still rewarding younger cattle for future weight gain, but the premium attached to that pathway has eased as seasonal conditions have deteriorated in some regions and supply has increased.

Historically, the spread between restocker and heavy steer indicators widens during herd rebuilding phases or when pasture conditions are strong. In 2019, the Heavy Steer Indicator averaged 288¢/kg lwt, while the Restocker Yearling Steer Indicator averaged 257¢/kg lwt, a spread of -31¢/kg lwt in favour of heavy steers. As seasonal conditions improved, restocker demand strengthened and the spread shifted to ‘positive’, where it has remained since.

What are the drivers?

Early in 2026, restocker demand started strongly, supported by producer confidence in grass supply and future weight gain opportunities. However, restocker demand throughout autumn has softened in some areas, while the heavy steer market has held up better (underpinned by the processing activity).

Dry conditions across parts of northern NSW – including the New England and North West regions – have been a key factor. Several months of below-average rain has limited pasture conditions and feed budgets are tightening due to increasing feed prices and fuel availability concerns. As a consequence, some producers are bringing cattle to market. This additional supply places pressure on restocker values.

At the same time, demand for finished cattle has remained well supported by processor activity and strong global demand for Australian beef. This has helped underpin the heavy steer market and narrowed the gap between the two indicators.

What to watch

The narrowing spread points to a more selective cattle market. Younger cattle are still attracting a premium, but that premium is becoming more sensitive to seasonal conditions, feed availability and confidence in future weight gain.

How weather conditions evolve over the coming months will be a key factor in whether this trend continues, particularly across NSW regions where feed availability is already influencing turn-off decisions.

Attribute content to: Emiliano Diaz – MLA Senior Market Information Analyst.

Information is correct at time of writing on 30 April 2026.