What impact will increased input costs have on Australian cattle farms?

Key points

- Cattle producers are exposed to increases in fodder and grain prices.

- Fertiliser, fuel, fodder and freight account for 23% of cattle farm costs.

- Farm cash costs for cattle producers are $408,000/year.

Fuel, fertiliser, fodder and freight (the four Fs) remain the dominant cost inputs across Australian broadacre agriculture. Recent analysis highlights these inputs and how potential changes could materially influence farm margins and production decisions, particularly in an increasingly volatile environment.

Impacts on total cash costs

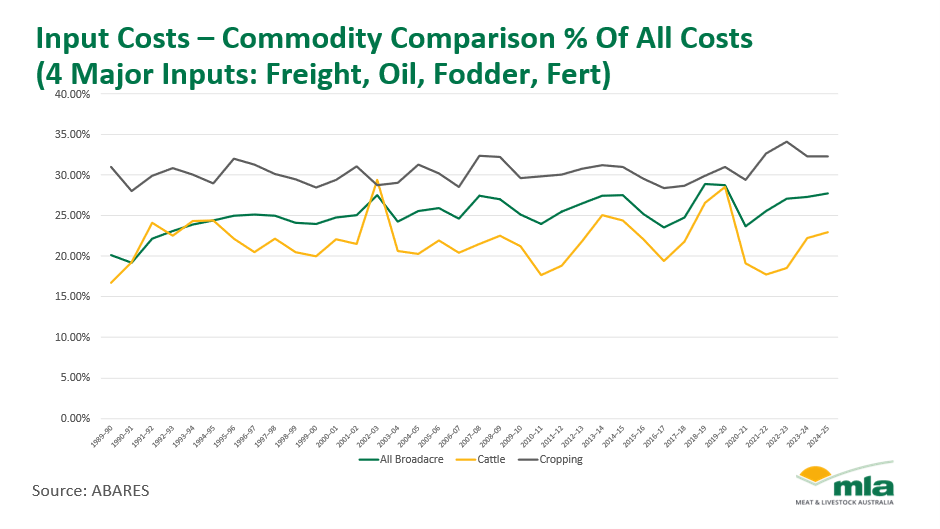

Across all Australian farms, the four Fs collectively account for approximately 27% of total cash costs. Fertiliser is the largest component at 13%, followed by fuel at 6%, with freight and fodder each contributing approximately 4%. On average, total farm cash costs now sit at roughly $738,000/year, based on long-term data from the Australian Bureau of Agricultural and Resource Economics and Sciences (ABARES) farm survey series, which dates back to 1990.

Over this period, average farm cash costs have more than doubled from $329,000 in 1990 to $738,000 in 2025 – representing a 124% increase. However, the cost structure varies significantly across enterprise types, which in turn shapes how exposed each sector is to movements in these key inputs.

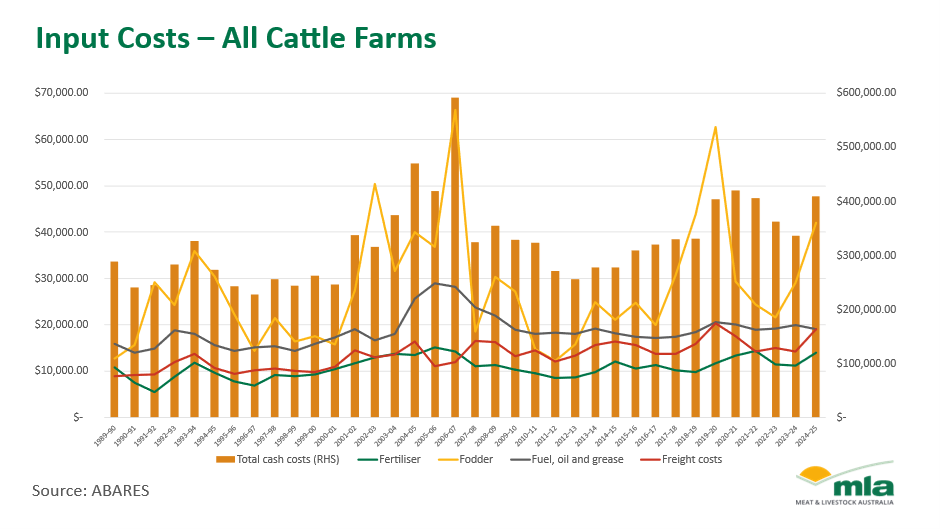

Fodder, freight and fuel pressures on cattle producers

For cattle producers, the cost profile is effectively inverted to that of cropping enterprises. Fodder and freight are the dominant pressures, rather than fertiliser and fuel. Average cattle farm cash costs are approximately $409,000, with fodder accounting for around $42,000, and both freight and fuel at roughly $19,000 each. Freight alone represents 4.6% of cattle farm costs, slightly above the broadacre average of 4.3%, reflecting the importance of logistics in moving livestock and inputs across large distances.

This divergence is critical when assessing the potential impact of geopolitical shocks, including the ongoing tensions linked to the Iran conflict, or weather conditions. While fertiliser and fuel is likely to see more immediate price pressure due to global supply chain disruptions and shipping constraints, the most significant risk to cattle producers lies in fodder.

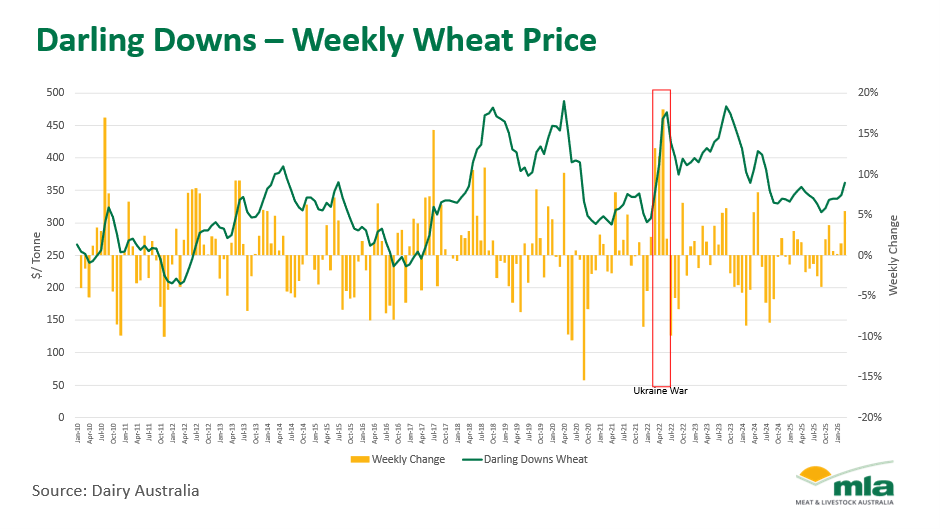

Feed grain prices are already trending higher. According to Dairy Australia data, Darling Downs wheat prices are currently around $361/tonne – the highest level since mid-2024 – and have recently recorded a weekly increase of 5%, the sharpest rise since May 2024. While prices remain below the peaks seen during the Russia-Ukraine war, the upward trajectory is clear.

For cattle producers, the key dynamic is timing. Increases in fertiliser, fuel and freight costs will initially be felt most acutely by cropping and mixed farming systems. However, if these higher input costs translate into reduced crop yields or tighter grain supply, the impact will flow through into higher fodder and feed prices. This lagged effect means cattle producers are likely to feel the full impact toward the back of 2026, following the 2026 winter crop harvest – when final tonnages are clear in Australia and globally.

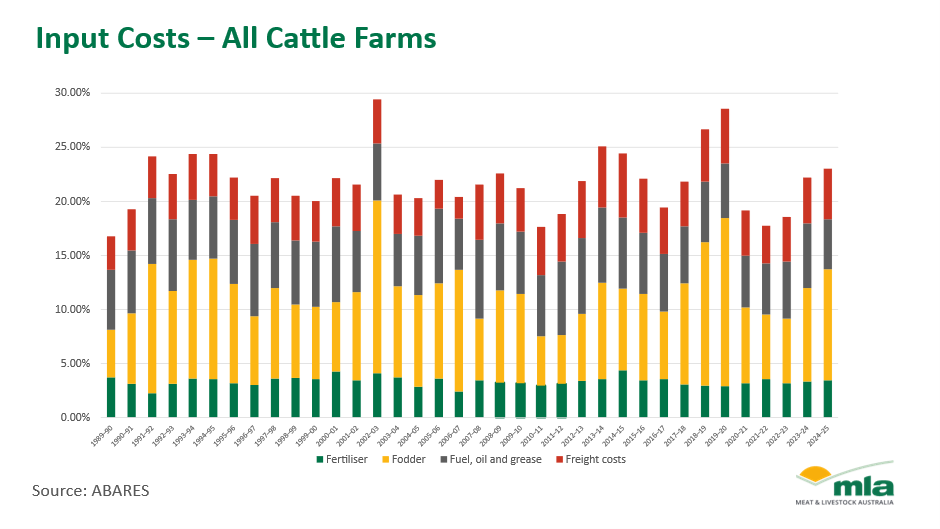

Importantly, while the four Fs account for a smaller share of total costs for cattle farms – around 23% compared to 32.3% for cropping farms – they remain a significant driver of profitability. Any sustained increase in these inputs will compress margins, particularly in an environment where cattle prices are beginning to ease due to emerging dry conditions in parts of NSW.

Freight is another critical watch point. Rising fuel costs could increase both the cost of moving cattle to market and the price of inbound inputs.

Attribute content to: Stephen Bignell, MLA Manager – Market Information

Information is correct at time of writing on 30 April 2026.