Australian lamb and mutton dominate global markets

Key points

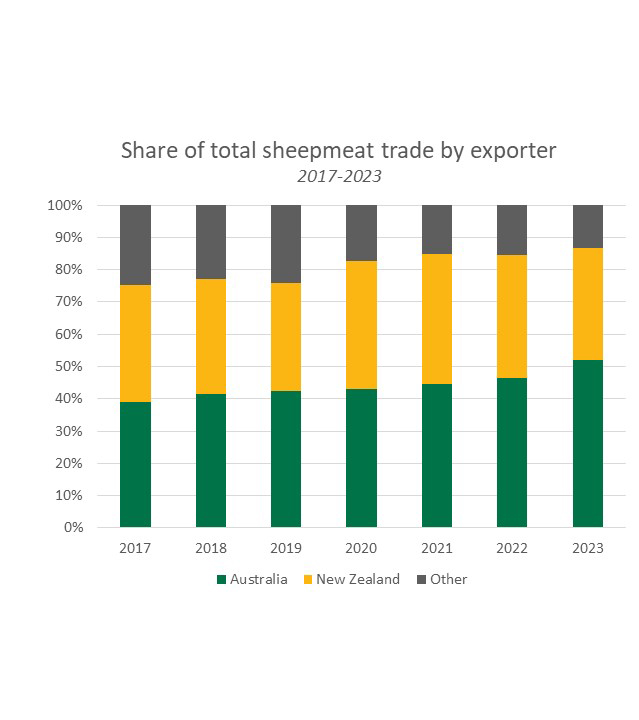

- Australian sheepmeat made up over 50% of total global trade for the first time in 2023

- Lamb and mutton market share in China grew, largely at the expense of New Zealand

- Australian sheepmeat remains well positioned to maintain strong export volumes in the international market.

With Australian lamb and mutton production reaching record highs, exports have lifted substantially, resulting in Australia accounting for over 50% of global sheepmeat exports in 2023 for the first time.

The large increase in exports has impacted our competitors, particularly New Zealand, the second-largest lamb and mutton exporting country. New Zealand’s exports have been affected by the increase in Australian supply, leading to a decrease in their market share in China. Additionally, supply chain constraints have hindered exporters’ ability to expand market share in other key markets.

China

China, being the largest market for sheepmeat by volume, experienced a 24% increase in total imports in 2023, reaching 429,434 tonnes.

Exports from New Zealand to China rose in 2023, but only by 10%. This meant that Kiwi sheepmeat accounted for 50% of Chinese imports in 2023, which is a considerable figure but well down on the 57% market share New Zealand held in 2023.

Instead, nearly all of the increase in Chinese imports came from Australia. Australian sheepmeat to China lifted by 43%, to 197,448 tonnes. This meant that 71% of the increase in China’s imports came from Australia, and Australia’s market share lifted to 46%, the highest figure on record.

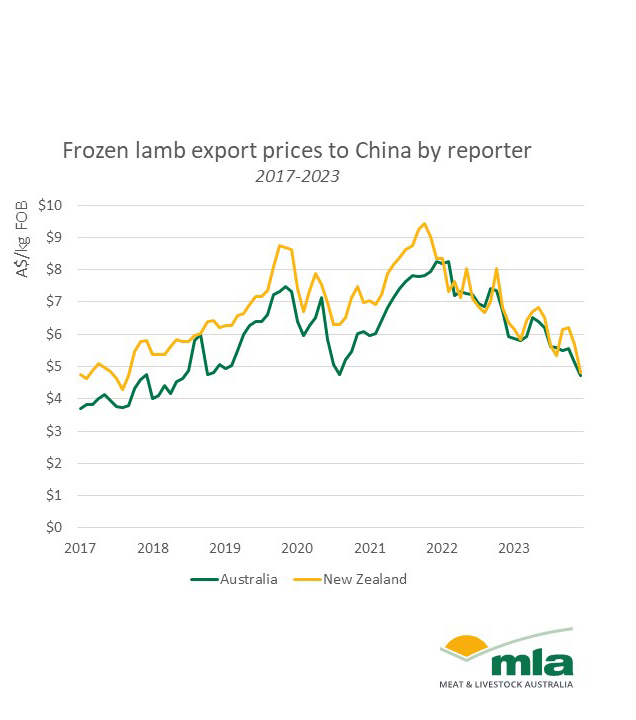

The rise in Australian market share has been accompanied by a shift in export pricing. Historically, New Zealand lamb held a $1-$1.30 premium over Australian lamb in the Chinese market. However, this premium has largely disappeared since around 2022, with both products now competitively priced, primarily influenced by fluctuations in the exchange rate.

Supply chain and storage

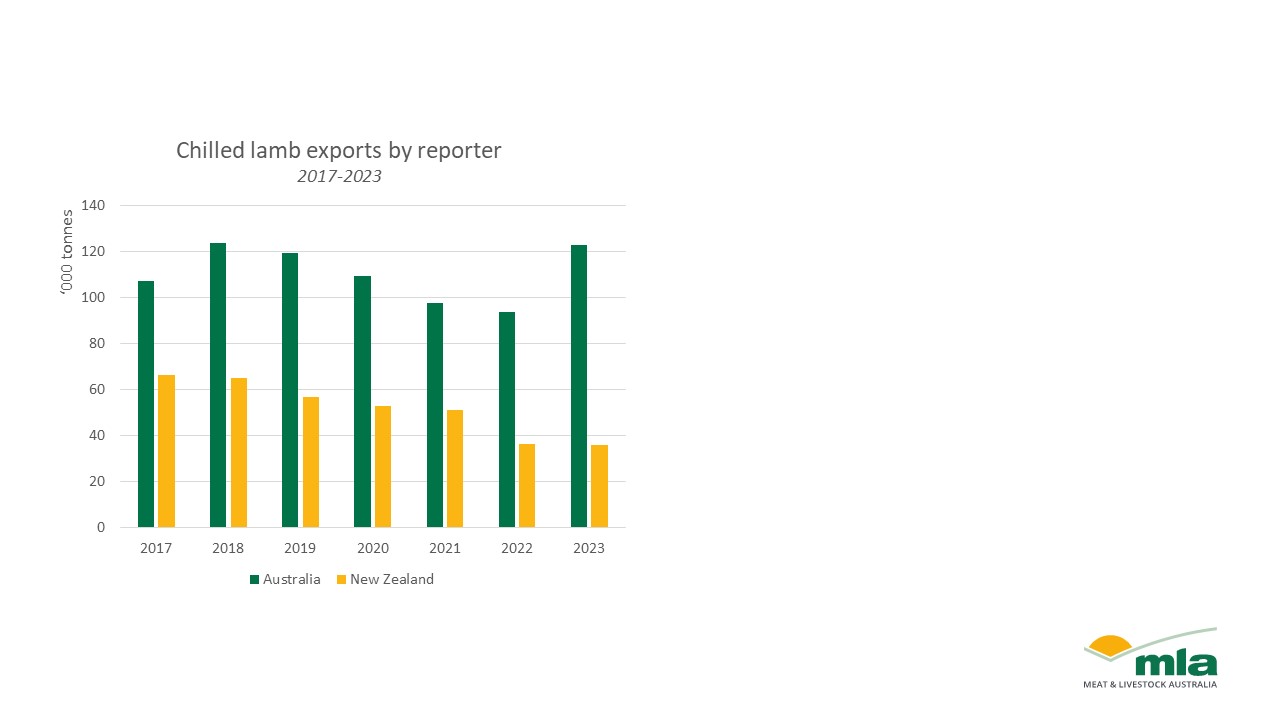

While New Zealand’s exports to China face pressure from increased in Australian supply, supply chain constraints have made it difficult for New Zealand’s ability to expand market share in other regions.

For example, Australian lamb exports to the Middle East and North Africa (MENA) lifted by 51% in 2023, totalling 58,516 tonnes, with chilled exports constituting 68% of that total. This rebound in chilled lamb exports after COVID-related supply chain disruptions has enabled Australian exporters to meet the demands in markets preferring chilled lamb, such as many in the MENA region.

In contrast, New Zealand’s exports of chilled lamb have been declining for several years, persisting through 2023, despite an overall increase in exports. This decline has prevented New Zealand from tapping into markets with a strong preference for chilled products, even during periods of high demand.