‘Restocker steer to heifer’ premium at highest level since the drought

Key points

- The ‘restocker yearling steer to restocker yearling heifer’ price premium mimics the natural cattle cycle and is based on drought-induced liquidation or herd rebuilding.

- At present, in actual terms, price premiums are at their widest level since the drought.

- With more heifers now on-farm due to the national herd rebuild, fewer producers are choosing to buy heifers at the saleyards.

Although prices for yearling steers are usually better than those for yearling heifers, the premium for restocker yearling steers has widened further in the last six months. This is largely due to the herd rebuild, meaning there is increased supply of heifers on-farm and producers are currently less inclined to buy heifers at the saleyards.

Price

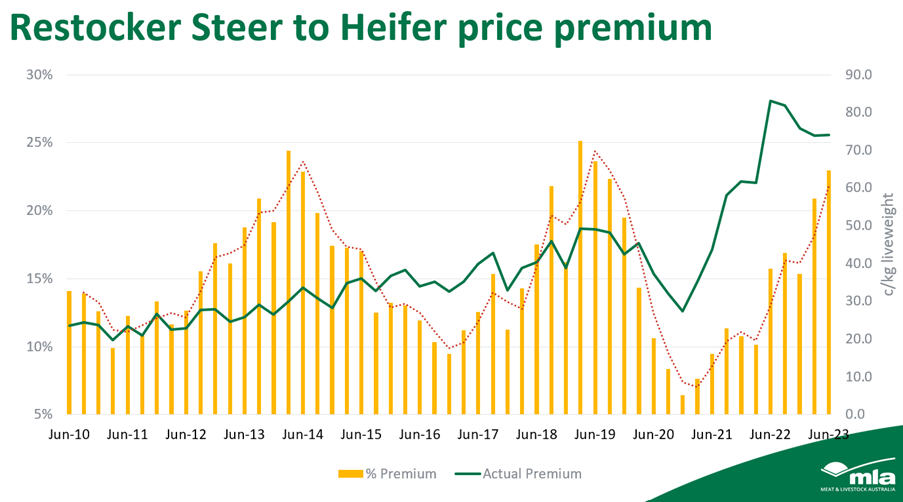

The restocker steer to heifer premium mimics the naturally occurring cattle cycle. Data indicates this premium reaches its widest point when cattle numbers have been rebuilt, or when drought-induced liquidation is at its most intense.

Looking at the quarterly price premium for yearling steers to yearling heifers since 2010, price premiums for steers are at their highest point (in percentage terms) since June 2019, now sitting at 23%.

In actual prices, restocker yearling steer prices in June 2022 reached an 83¢/kg liveweight (lwt) premium on average to restocker yearling heifers – a new record. Despite softening in the actual price premiums, the percentage increase has been rising since December 2020 and has risen sharply over the last six months (Figure 1).

Figure 1. Restocker steer to heifer price premium (2010-2023)

Source: MLA

According to historical data, the previous two years when premiums were at their highest were 2014 and 2019 – both years when the cattle herd was in liquidation during droughts.

Larger calf drops as a result of higher female retention (the female slaughter rate hit its lowest level in 50 years in 2022) is evidently reducing buyer demand and therefore placing downward pressure on the prices of restocker yearling heifers. With more heifers on-farm, producers are less inclined to purchase heifers at the saleyards – a trend that will see the national herd transition from a rebuild to a growth phase.

Supply

Analysis of national year-to-date yarding volumes suggests heifers continue to be retained intensely, relative to other categories and total national performance:

- Year-to-date restocker yearling heifer yardings are firm year-on-year.

- Overall yearling heifer yardings have risen by 5% or 4,000 head.

- Processor-bought yearling heifers have increased by 24.3% or 2,701 head.

- Total national yardings are higher in year-to-date terms are higher by 20,000 head or 4%.

It’s evident that the supply of restocker yearling heifer volumes is trending lower than the general national performance.

This data partially explains the current price premium for steers being so high and demonstrates two things:

- Producers are selling their second drafts of heifers, meaning secondary quality animals are being offered for sale which is placing downward pressure on heifer prices.

- Higher volumes of processor-bought heifers (relative to the category) suggest producers have rebuilt their female base and lack the need to retain more heifers than they have previously.

As producers are retaining the top of the drafts to ensure the future of their breeding herd is of the best genetic and productivity base, secondary quality animals offered to market will be contributing to lower price points for restocker heifers. Furthermore, the need for buyers to compete heavily on restocker females has waned due to the rebuild.

Looking ahead

In current terms, the price premium for restocker steers relative to heifers may continue to widen in the coming months due to the hastened pace of the herd rebuild and transition to a growth phase.

Larger calf drops and therefore increased turn-off rates will ensure a large supply of yearling heifers in the market. This means a continuation of downward price pressure on restocker yearling heifer articles.

This dynamic will change with seasonal conditions and, due to this, certain regions will have stronger herd rebuilds or growth than others. At present, Queensland’s herd rebuild is continuing and demand for restocker yearling heifers remains strong.