Trade lamb premium surges as supply tightens

Key points

- Trade lamb extends its margin over heavy lambs by 95¢/kg cwt, the highest in more than five years.

- Trade lamb yardings remain well below average, while heavy lamb supply has held firm.

- Softer demand from some export markets and reduced processing capacity are limiting further price gains.

Season and supply

Favourable seasonal conditions and strong pasture growth across key southern sheep-producing regions have enabled producers to focus on weight gain while also capitalising on record lamb prices. As a result, there has been a noticeable shift towards heavier sale weights coming through saleyards compared with previous years.

The strong economic incentive to finish lambs to heavier export weights has reduced the availability of trade and lighter-weight lambs, increasing the trade lamb premium to 95¢/kg carcase weight (cwt) for the week ending 10 July.

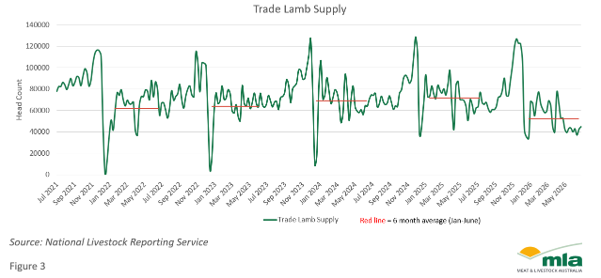

Figure 2 highlights the decline in trade lamb supply relative to the five-year average during January to June 2026. Weekly trade lamb throughput has averaged around 55,000 head in 2026, well below the historical average of 65,000 head, indicating a notable tightening in supply during the first half of the year.

In contrast, heavy lamb throughput has remained broadly in line with historical levels. Weekly heavy lamb yardings have averaged 50,000 head in 2026, compared with the five-year average of 45,000 head.

The relatively stronger supply of heavy lambs compared with trade lambs, has likely contributed to the widening price differential between the two categories.

Global demand and processing

The widening price gap has also been influenced by softer demand from some export regions such as the Middle East and North Africa. Exports to these markets were down 35% year-on-year (YoY) in June, compared with an overall decline of 10% YoY in total lamb exports.

Increased price sensitivity in some markets, driven by higher meat prices and rising logistics costs associated with trade disruptions, has weighed on demand for export lamb. At the same time, reduced processing capacity has limited competition as processors continue to face margin pressure from elevated livestock purchase costs.

Looking ahead, lamb prices are likely approaching their cyclical peak as supply nears its seasonal low, processing capacity remains constrained, and some export markets struggle to absorb current price levels. This week, prices eased slightly for both trade and heavy lambs, declining 37¢ and 16¢/kg cwt, respectively.

However, demand fundamentals remain strong, particularly in premium export markets, which should continue to provide a firm floor for lamb prices. Supply availability and processor capacity are expected to remain the primary drivers of price movements in the months ahead.

Attribute content to: Stuart Bull, MLA Market Information Manager.

Information is correct at time of writing on 17 July 2026.