Restockers challenge feedlots for young steer supply

Key points

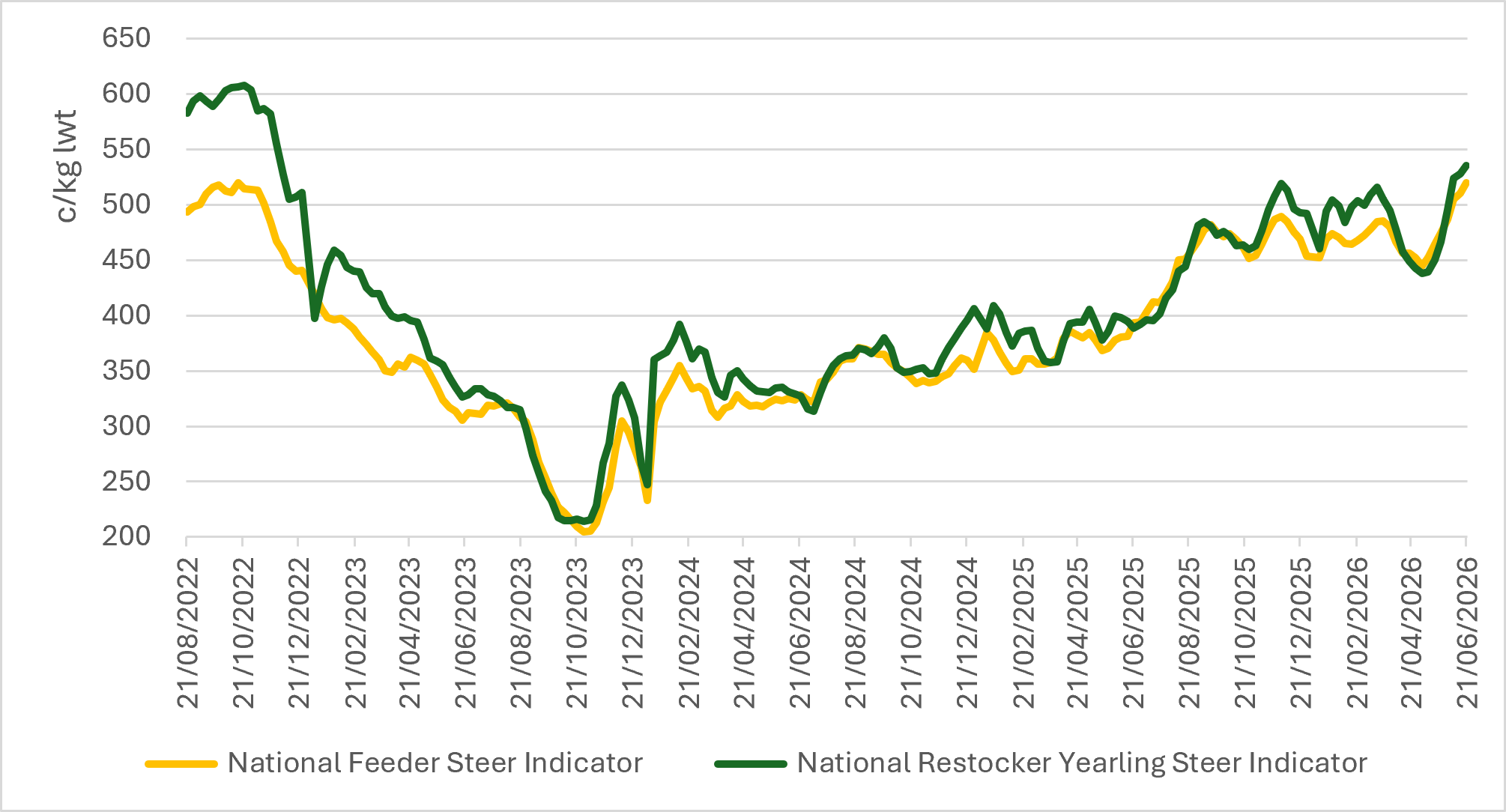

- Restocker yearling steers have lifted close to 100¢/kg lwt, while feeder steers have gained more than 70¢/kg lwt since April.

- Restocker yearling steers maintained a premium over feeder steers as grass and grain buyers competed for the same cattle.

- Competition is strongest across the 280–400kg range, with Queensland providing volume and NSW driving much of the price strength.

Restockers continue to drive the overall cattle market due to strong competition between backgrounders and feedlots, with both buyer groups competing for a tighter supply of young cattle.

The National Feeder Steer Indicator lifted 25¢ to 530¢/kg liveweight (lwt), while the National Restocker Yearling Steer Indicator rose 3¢ to 530¢/kg lwt. They both overcame the recent peak earlier this month and set a new high (since 2022).

The move kept restocker yearling steers at a premium to feeder steers, with the spread sitting around 15¢/kg lwt. Feedlots continue to provide a firm price floor, but restockers are now setting the pace, particularly where seasonal confidence has improved.

Since late April, restocker yearling steers have gained a significant 100¢/kg lwt, while feeder steers have also lifted 94¢/kg lwt. This marks a clear shift from April, when dry conditions and larger offerings weighed on restocker confidence.

The market has moved from a feeder-led base to a more competitive environment where grass and grain buyers are bidding into the same steer pool. Feedlot demand remains firm, supported by ongoing grainfed turn-off requirements, but the return of restocker demand has accelerated the price recovery.

Weight range competition

The weight profile shows where competition is strongest. Feeder demand remains concentrated in heavier lines, particularly 330–400kg and 400kg-plus cattle. These weights accounted for most feeder steer throughput this week, confirming feedlots are still focused on cattle that can move efficiently into grain programs.

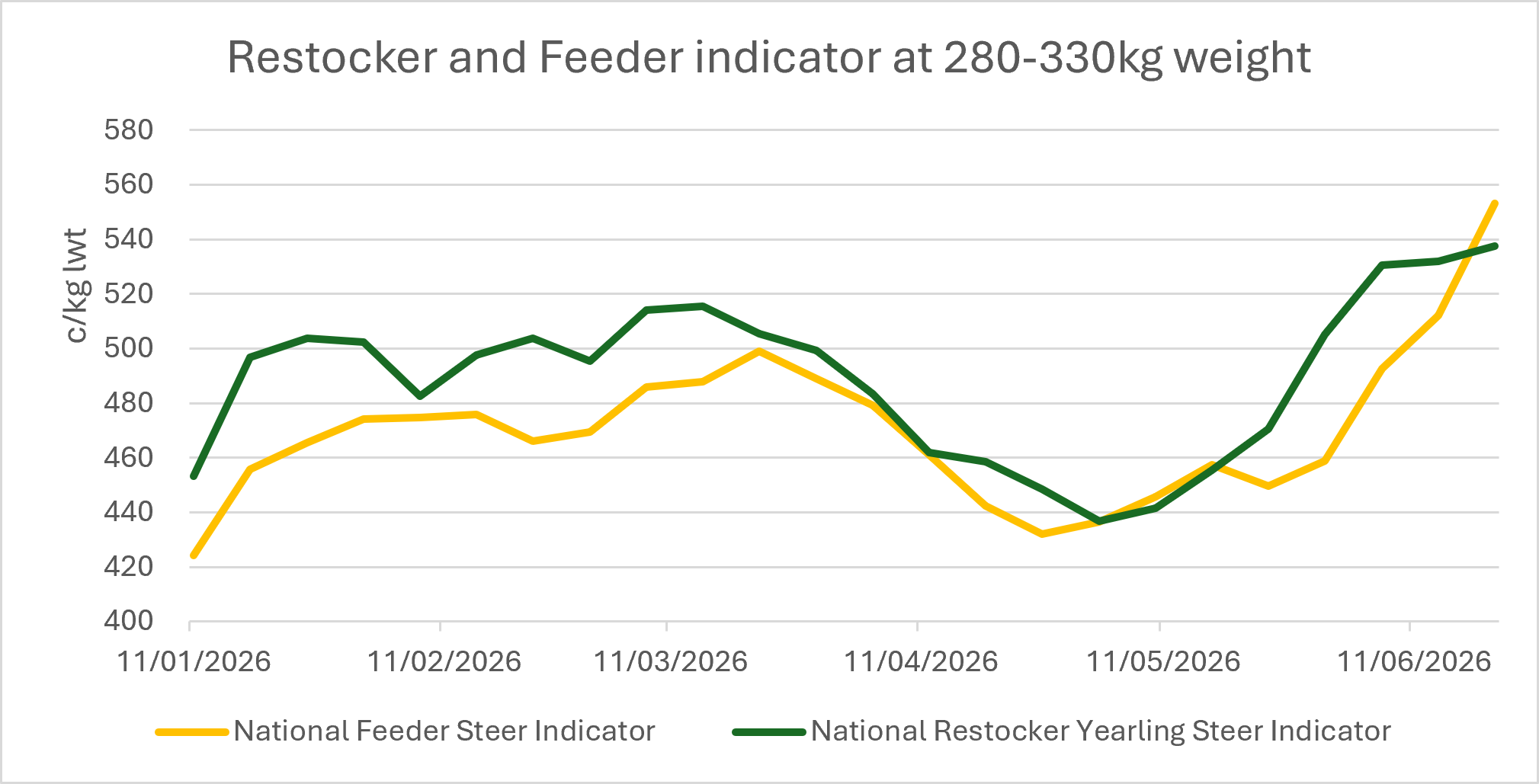

However, the lift in lighter feeder categories suggests buyers are reaching further down the weight range where supply is tight. The 280–330kg feeder segment recorded one of the strongest weekly price movements, albeit off a smaller offering. This points to feedlot buyers competing more actively for cattle that would otherwise have attracted restocker interest.

Restocker demand was more evenly spread across 200–400kg cattle, with the strongest volume in the 200–280kg range. The 330–400kg restocker category also held firm, trading at the highest average price across the restocker weight ranges. This demonstrates that restockers are not only chasing lighter cattle to put back on grass but are also prepared to compete for heavier yearlings with more production flexibility.

The overlap is most evident in the 280–400kg range. These cattle can suit either pathway depending on frame, condition, feed availability and buyer margins. Restocker values holding above feeder values suggest backgrounders are currently prepared to outbid feedlots for the right animal.

Queensland supplies the numbers, while NSW drives price momentum

Queensland continued to provide the volume base, particularly through Roma, Blackall, Dalby and Gracemere. In the restocker yearling steer market, Roma was the dominant contributor this week, accounting for more than one-third of throughput and trading above the national average. Blackall also supported the indicator, with prices lifting despite a smaller yarding.

The restocker indicator was supported by stronger results through Roma and Blackall, alongside high-priced lines at Wagga.

For feeder steers, Queensland supplied depth, but NSW provided much of the price strength. Blackall, Dalby and Roma were the largest volume contributors, while Wagga, Carcoar, Gunnedah and Tamworth all traded well above the national average. Gunnedah and Carcoar recorded some of the strongest week-on-week price improvements, while Wagga added both volume and price support.

Attribute content to: Emiliano Diaz, MLA Senior Market Information Analyst.

Information is correct at time of writing on 17 June 2026.