MLA’s latest cattle and sheep projections released

This week, Meat & Livestock Australia (MLA) published the first 2024 cattle and sheep industry projections for 2024.

These industry projections offer a comprehensive outlook of the cattle and sheep sectors, presenting three-year forward-looking forecasts for the national herd and flock, slaughter, production, and carcase weights for cattle, lamb and sheep/mutton. The forecasts are accompanied by detailed analyses of domestic and global factors, encompassing macro-economic elements and supply and demand dynamics.

The MLA Market Information team will be hosting webinars to present the February release of the Cattle Industry Projections and Sheep Industry Projections. These webinars will delve into the findings of the documents, and attendees will have the opportunity to pose questions to the Market Information team regarding the Projections document and its associated values.

Click the following links to register for the webinars:

- MLA Cattle Industry Projections Webinar, Tuesday 12 March, 10 am AEDT: Register here

- MLA Sheep Industry Projections Webinar, Tuesday 19 March, 10 am AEDT: Register here

Cattle projections

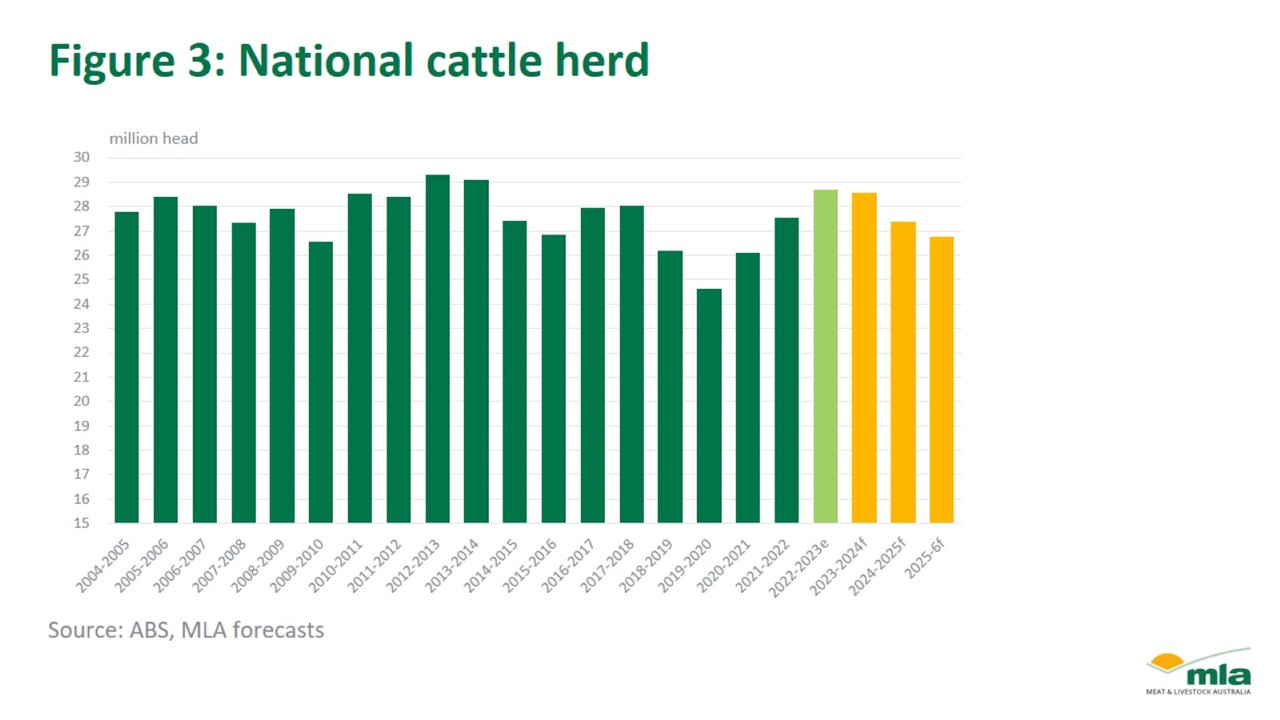

Herd size

The Australian cattle herd is anticipated to decrease marginally by less than 1% to 28.6 million head by 30 June 2024. The increased turn-off observed throughout 2023 and into 2024 has been primarily influenced by high supply rather than producer intention to destock. This suggests that the national cattle herd is transitioning into a maintenance phase. While female retention remains above long-term averages in Northern production systems, it falls below long-term benchmarks in southern systems.

Slaughter and production

MLA projections indicate a rise in slaughter, with an 11.7% increase expected in 2024, reaching 7.9 million head, the highest since 2019. This elevated processor-ready supply is projected to persist throughout 2024 as the herd matures. Looking ahead, slaughter rates are forecasted to increase again in 2025 before plateauing into 2026. The heightened slaughter rates will consequently lead to increased beef production, forecasted to rise by 10.8% to 2.5 million tonnes in 2024. Despite a slight dip in carcase weight, the elevated slaughter will sustain high levels of beef production.

Global

The United States remains Australia’s primary supply competitor, exporting beef to key markets shared with Australia. The US has forecasted an improvement in drought conditions across key cattle-producing regions, potentially initiating an extensive herd rebuild within the year. This anticipated contraction in American supply due to rebuilding represents an opportunity for Australian beef in global markets.

Sheep projections

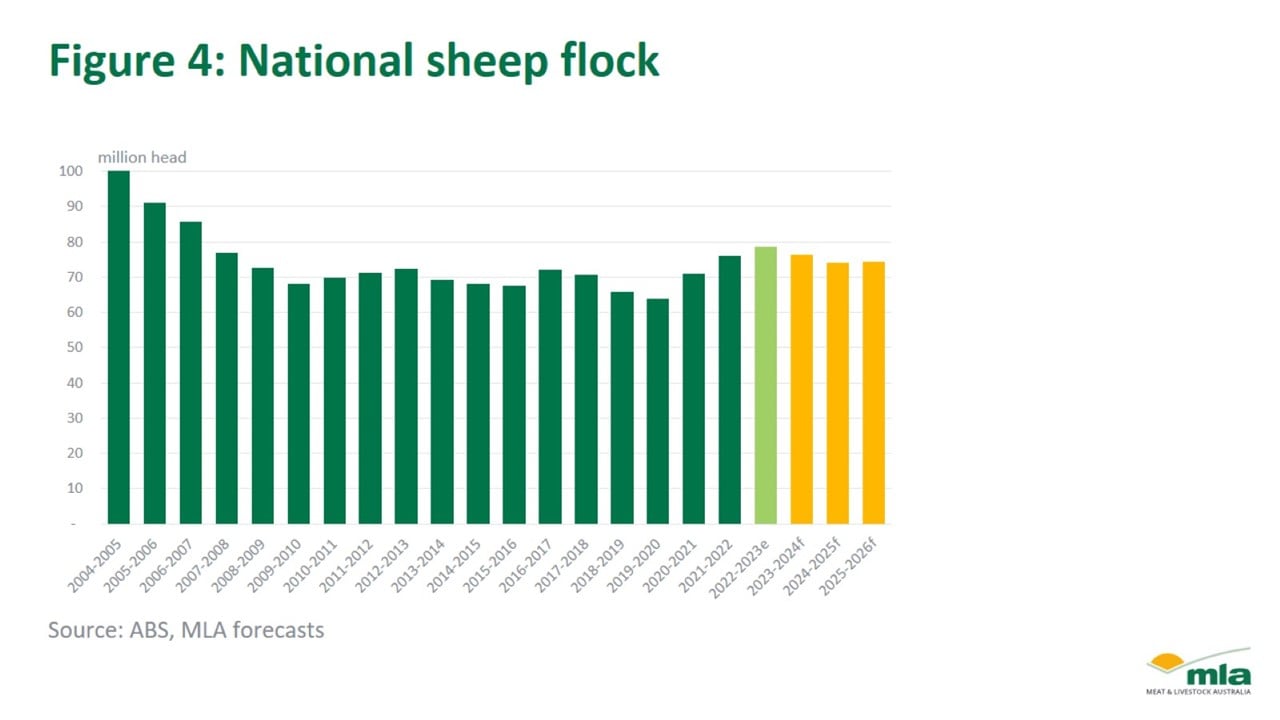

Flock

The Australian sheep flock is projected to decrease by 2.9% to 76.5 million in 2024. Producer emphasis on productivity and genetics in the sheep flock has resulted in impressive marking rates over the last few rebuilding years. Despite the anticipated contraction over the next few years, the flock is not expected to undergo a substantial destocking phase and is forecasted to remain above the 10-year average for the foreseeable future.

Slaughter and production

High supply has created an environment where the transition from favourable weather conditions to average conditions has led to increased slaughter rates in 2023. The high slaughter rates observed in the early months of 2024 indicate a further increase in slaughter to 26.1m head (lamb) and 10.1m head (mutton), before easing in 2025 and 2026. This elevated slaughter will result in peaks in sheepmeat production in 2024, leading to record levels of Australian sheepmeat entering the global market. Lamb production is projected to increase by 9% to 621,000 tonnes in 2024, while mutton production is expected to rise by 3.1% to 254,000 tonnes. This follows Australia’s record lamb production in the calendar year 2023, with 599,461 tonnes of lamb produced.

Global

As the largest exporter of sheepmeat, increased Australian production will contribute to higher volumes of globally traded sheepmeat. Economic resilience in the USA and emerging markets will drive demand for lamb, despite uncertain consumer demand outlooks in China. Nevertheless, a shortage of competing proteins will encourage imports of sheepmeat in high protein consumption markets.