Increase in supply impacts co-products

Key points

- Cattle and sheep slaughter has remained consistently high in 2023, supported by an easing in the market with the increase in supply.

- The supply increase has improved availability of co-products and placed pricing pressure on the market.

Supply and slaughter

Cattle and sheep supply have been steadily increasing with consistently high yardings.

The maturity of the southern rebuild has brought more cattle online and through saleyards. Year-on-year national yardings to date have increased 6% or 22,620 head.

Southern yardings (NSW, SA, Tasmania, Victoria and WA) have increased 16% year-to-date. In Queensland, yardings are back 10% year-on-year due to a later rebuild phase and the recent flooding and wet weather in the central and northern regions, which has caused a tightening of supply.

Sheep and lamb yardings paint a similar picture with a 50% and 11% increase year-to-date respectively. Favourable seasonal conditions and successive high lamb drops have helped to support these increases.

The latest Sheep Producer Intentions survey also points to an increase in supply in the coming months.

This supply has placed downward pricing pressures on the market, allowing processors to purchase livestock at more affordable prices than the records seen at the beginning of last year.

Slaughter rates have been significantly higher year-on-year. Due to the flooding at the beginning of 2022, some processing plants had limited numbers of stock processed. Comparatively, Queensland, NSW and Victorian cattle slaughter remains at elevated levels in 2023.

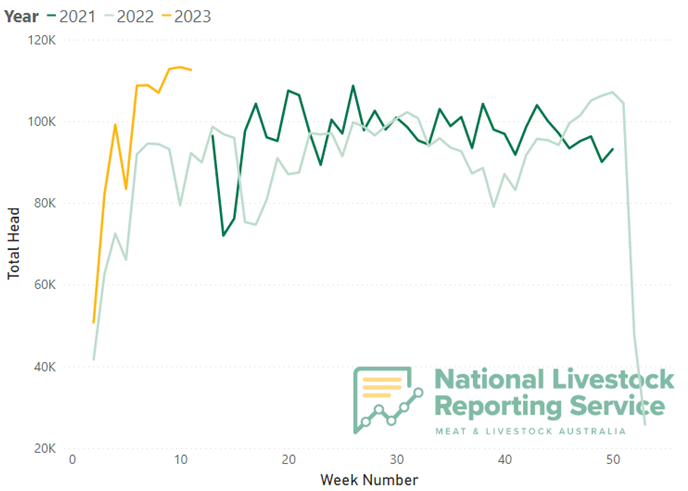

National cattle slaughter was at 112,574 head, or 22%, above year-ago levels last week (Figure 1). Increased levels of slaughter have been supported by supply and the price of processor cattle easing in recent weeks.

Figure 1: National cattle slaughter

Source: Meat & Livestock Australia

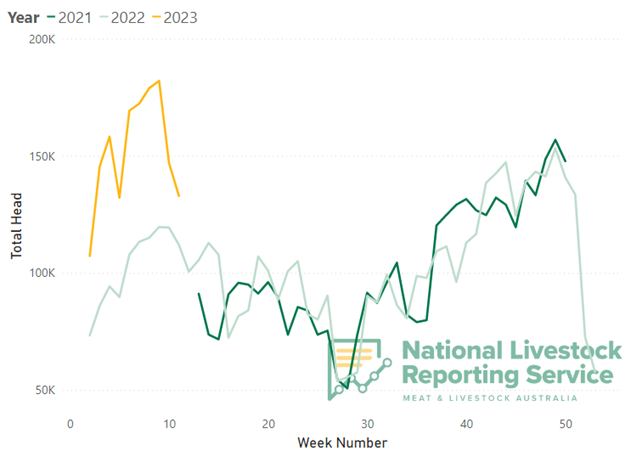

Sheep slaughter peaked at the end of February at 182,059 head, 52% above 2022 numbers. Sheep slaughter has remained consistently above 2022 numbers as more stock comes online (Figure 2).

Figure 2: National sheep slaughter

Source: Meat & Livestock Australia

Last year, sheep and lamb processors’ capacity was more consistent, even with public holidays or flooding conditions. Small stock is easier to transport across state boarders and processing is more automated.

Co-product prices

Many of the co-products that MLA report on have eased in price according to the March 2023 co-product market report. Many beef co-products that were reaching records at the end of last year have eased significantly. Cheek meat has seen a 25% softening in price month-on-month after reaching records at just over $12/kg in September 2022. The increasing popularity of the cut as beef prices rose helped to support these high prices.

Halal lungs have followed a similar trend with consistently high prices over 2021 and 2022, at around $5/kg. Prices have been easing since August last year and softened a further 8.6% this month.

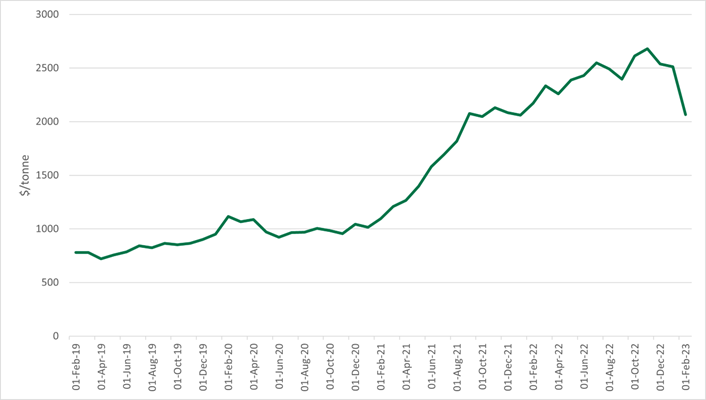

Rendered products such as cattle tallow, which is a key component of biofuels, reached its peak at the end of November 2022 of $2,680/tonne but has now softened to $2,007/tonne (Figure 3).

Figure 3: Cattle tallow prices

Source: Meat & Livestock Australia

The increasing supply of processor cattle, and the ability for buyers to purchase them at lower prices, leaves room for the further processing of co-products. Increased supply of these products places pricing pressure on the market.

Sheep co-products have been mixed this month. With the increase in supply on the market, heart and tripe eased 34% and 44% respectively. Other products, such as kidneys, performed quite well averaging to $5.33/kg, a 10% lift on last month.